Weekly Market Update: 3 December 2025

Markets Bounce Back

After dipping entering December, we’ve seen a strong rebound across the crypto market. Bitcoin flushed to $83K before recovering sharply back toward $92.5K, now attempting to reclaim the key resistance zone around the yearly open at $93K. Ethereum has also stabilised, holding the $2.8K support and reclaiming the $3K level as broader market sentiment turns green. The tone remains cautious, but price action has improved meaningfully from last week’s lows.

We are one week from the next Federal Reserve meeting, and the macro backdrop has shifted. Two weeks ago, markets priced only a 22% chance of a December rate cut, that figure has now surged to 93% ahead of the December 10 decision. At the same time, President Trump introduced Kevin Hassett as the “potential next Fed Chair,” with an official pick expected early next year. Hassett remains the frontrunner with roughly 85% odds, and a Fed chair leaning toward earlier and faster cuts is seen as broadly supportive for risk assets, including crypto.

Institutional Adoption Accelerates

Institutional adoption took a meaningful step forward as Vanguard, the $11T AUM giant that publicly rejected Bitcoin ETFs in 2024, fully reversed course and opened spot BTC, ETH, SOL, XRP, and HBAR ETF trading to its 50 million clients today. The impact was immediate, Bitcoin jumped roughly 6% around the U.S. open on the first day the platform lifted its ETF ban, signalling how much demand was waiting for access. Flows confirmed the magnitude. BlackRock’s IBIT saw nearly $1B in trading volume within the first 30 minutes of availability to Vanguard clients, a reflection of both pent-up demand and the depth of institutional rails now supporting BTC.

On the same day, Bank of America, the US second largest bank moved to allow 15,000 wealth advisers to recommend Bitcoin within a 4% allocation for its $3.1T client base, which is up to $124B in potential crypto exposure. Together, these two announcements represent one of the largest single day shifts in mainstream access to digital assets we’ve seen, showing how rapidly crypto is being integrated into traditional portfolio construction.

QT Officially Ends

The Federal Reserve officially ended its three-year quantitative tightening program on December 1, a meaningful shift in the global liquidity regime that has gone largely unnoticed in crypto. QT has quietly been one of the biggest headwinds for markets over the past two years, effectively pulling liquidity out of the system and slowing risk-asset momentum. That period has now ended. By stopping the balance sheet runoff, the Fed has halted the liquidity drain that contributed to tighter funding conditions throughout this cycle.

For crypto, this matters because digital assets remain the most liquidity sensitive asset class. When liquidity contracts, rallies fade, when liquidity begins expanding, risk appetite improves. Ending QT doesn’t flip markets overnight, but it does mark a directional shift from liquidity withdrawal toward eventual easing. Historically, these pivots have helped markets stabilise, offering a more constructive backdrop as we move into Q1 2026. It’s one of the more important macro developments of the year, even if it sits in the background while attention remains focused on week to week price action.

Microstrategy Cash Reserve + Selling BTC?

MicroStrategy has raised a $1.44 billion USD cash reserve to fund approximately 21 months of dividends and interest payments, estimated at $750–800 million annually, while holding 650,000 BTC (~3.1% of total supply) at a $74,436 average cost. CEO Phong Le has explicitly outlined conditions for selling Bitcoin, framing it as a contingency in the toolkit rather than ideological abandonment. BTC sales become justified if the stock valuation trades below its BTC value (mNAV < 1x) and capital markets shut or become prohibitively expensive. Current analysis suggests mNAV is trading around 1.1x, meaning stress levels (~0.9x) are within reach in volatile markets. If Bitcoin falls and stays depressed while MSTR trades at a persistent discount to BTC NAV, the board faces a trilemma. Skip dividends (damaging creditworthiness), issue equity at a steep discount (massive dilution), or sell BTC (extending runway while maintaining credit reputation). The $1.44B reserve delays this reckoning, but if BTC prices remain low and capital markets tighten for 12+ months, the reserve depletes and arithmetic forces BTC sales to avoid default. Since MicroStrategy controls 3.1% of total Bitcoin supply, any material liquidation would significantly impact market liquidity and sentiment during stress periods.

Bloodbath November

November 2025 has been one of the most devastating months in cryptocurrency history, with Bitcoin plunging 33% from its October peak and over $1 trillion in total crypto market capitalisation being wiped out, record breaking liquidations and ETF outflows and the Crypto Fear and Greed Index hitting “Extreme Fear” (11), triggering a flywheel of panic across digital asset markets. BTC broke the critical support range around USD $92,000 - $94,000 and spiraled down to nearly USD $80,000. If the downtrend continues, BTC might hit the next major support zone between USD $74,000-$76,000 before the next uptrend.

The Bitcoin ETF, Blackrock’s IBIT, suffered over $2 billion in outflows despite becoming BlackRock’s highest-growing product category. The fund’s AUM dropped from $100 billion in October with BTC hitting an all-time high, to around $70 billion in November.

Despite October ending on a green candle, the optimism that carried into November quickly evaporated amid deteriorating macroeconomic conditions. Fed rate cut expectations faded as inflation remained stubborn around 3% and officials grew cautious about easing too soon, creating tight liquidity and subdued risk appetite across risk assets. Adding to the pressure, uncertainty from Trump's tariff announcements in October had already triggered a $19.3 billion liquidation event in late October, marking the largest liquidation cascade in cryptocurrency history. That initial shock left leverage elevated heading into November, priming the market for another capitulation when macro data disappointed.

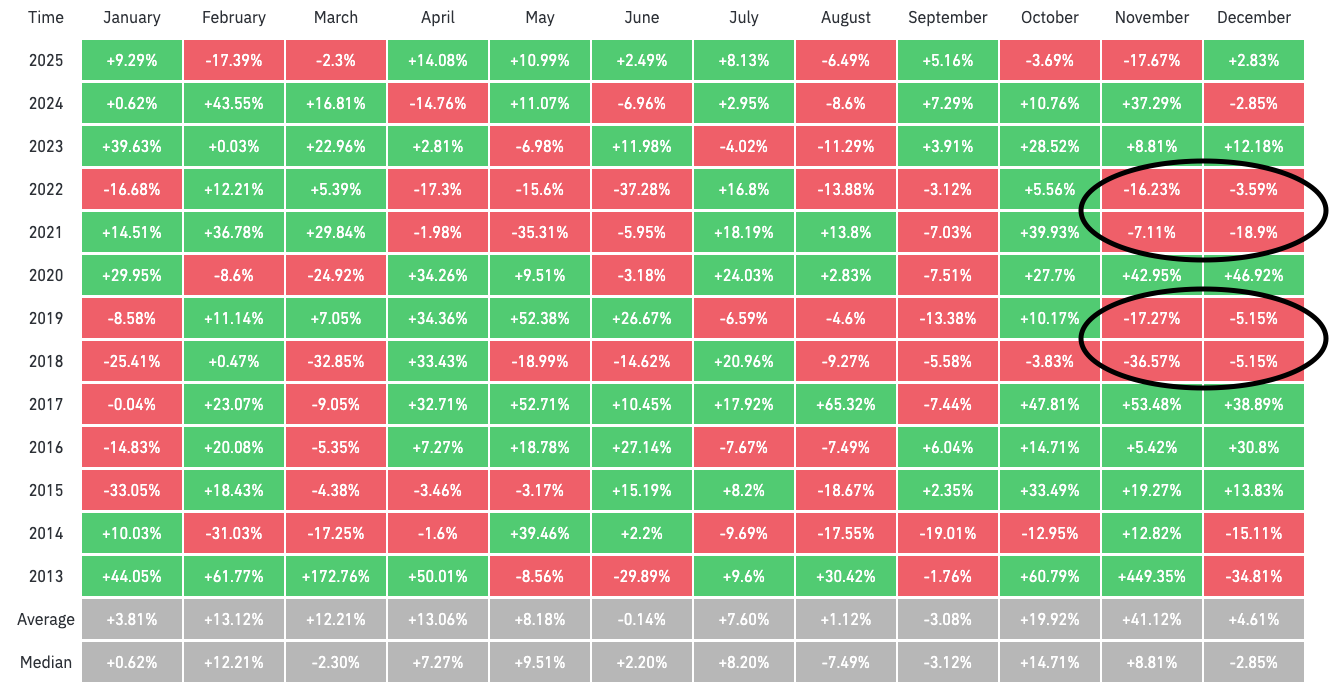

Historically, Bitcoin's November performance has been more bullish, showing either strong double-digit gains or at least mildly positive results in the vast majority of years. When November does turn red, it almost always follows a period of elevated gains earlier in the year and tends to occur alongside broader de-risking and macro stress rather than isolated cryptocurrency weakness. November closing on a monthly red might reflect an inflection point where momentum reverses rather than temporary noise. In prior years where November weakness materialised, the selling typically bled into December rather than resolving quickly, as forced liquidations, tax-loss harvesting, and persistent risk-off positioning continued.

The unusual nature of a negative November does not automatically guarantee deeper losses ahead, but it meaningfully raises the odds that selling pressure persists into December. Historically, cryptocurrency markets have often needed time to stabilise after this kind of late-year pullback, with a proper bottom or renewed strength appearing only after year-end capital flows and institutional rebalancing reset in January.

Japan Carry Trade Unwind

The yen carry trade is becoming relevant again as Japan moves away from decades of near-zero rates while the U.S. shifts toward easing. For nearly 20 years, some of the world’s largest funds relied on Japan, borrowing yen at close to 0%, converting it into dollars, and deploying into higher-yielding assets across equities, bonds, emerging markets, and increasingly, crypto. As rate differentials tighten, those institutions are being forced to unwind positions, sell assets, and repay yen-denominated debt. That process drains liquidity globally and has likely contributed to the recent risk-off move in digital assets.

A similar dynamic played out in mid-2024, when the Bank of Japan delivered its first meaningful rate hike in almost two decades. Markets were positioned for stability, not tightening, and the sudden shift forced a rapid unwind of yen-funded trades. Crypto absorbed that shock immediately, Bitcoin fell roughly 30%, but the move ultimately functioned as a clean leverage flush rather than a broader breakdown. Once forced selling cleared, the announcement day itself marked a major local bottom.

We are now within a week of the next potential policy shift, with markets pricing a high probability of a BoJ hike alongside a Fed cut in December, the exact combination that narrows the carry trade and pressures large allocators to de-risk. The difference this time is that the move is widely expected and better communicated, meaning the liquidity drain is likely already priced in. Could we again be approaching a local bottom as policy clarity approaches?

Kane Bisogni

.jpg)

Bitcoin Vs XRP: What Separates Them (And Why Investors Care)

Weekly Market Update: 18 March 2026

Weekly Market Update: 11 March 2026

Weekly Market Update: 04 March 2026

Weekly Market Update: 25 February 2026

.jpg)

Crypto vs Stock Trading: Which Is The right Investment For You in 2026

.jpg)

How to Buy XRP in Australia: A Complete Guide for Beginners in 2026

Weekly Market Update: 18 February 2026

Weekly Market Update: 11 February 2026

Weekly Market Update: 04 February 2026

Weekly Market Update: 28 January 2026

What Does Liquidity Mean in Crypto? A Beginner’s Guide

%20(1).jpg)

How to Build a Diversified Crypto Portfolio

Weekly Market Update: 21 January 2026

Weekly Market Update: 14 January 2026

The Best Crypto Brokers and Trading Platforms for 2026

Weekly Market Update: 07 January 2026

Weekly Market Update: 24 December 2025

Weekly Market Update: 17 December 2025

Weekly Market Update: 10 December 2025

Weekly Market Update: 3 December 2025

Weekly Market Update: 26 November 2025

Weekly Market Update: 19 November 2025

Weekly Market Update: 12 November 2025

.jpg)

SMSF Crypto Investing Australia: A Complete Guide

Weekly Report 5th Nov

DeFi Explained: How Decentralised Finance Is Changing Traditional Banking (Australia, 2025 Edition)

.jpg)

Our Guide to Meme Coins in 2026: How to Pick a Winner

.jpg)

Smart Contract Hacks Australia: How Exploits Happen and How to Protect Your Crypto

.jpg)

Institutional Money in Crypto: How Big Investors Are Changing the Game

.jpg)

Crypto Outlook 2025: Has the Bull Market Been Interrupted or Just Reset?

.jpg)

How Crypto Is Changing the Way We Buy Luxury

.jpg)

Real-World Assets (RWA): The Dominant Crypto Sector of 2025

.jpg)

Crypto Market Manipulation: How Liquidity Squeezes Shape the Market

Weekly Market Update: 22 October 2025

Weekly Market Update: 8 October 2025

Weekly Market Update: 15 October 2025

.jpg)

Crypto Scams Australia: A Beginner’s Guide to Safe Investing

Weekly Market Update: 1 October 2025

Weekly Market Update: 24 September 2025

Weekly Market Update: 17 September 2025

Weekly Market Update: 10 September 2025

Buying Cryptocurrency as a Company: Everything You Need to Know

How to Buy and Sell Large Amounts of Cryptocurrency (Including Bitcoin, XRP, ETH) in 2026

Weekly Market Update: 3 September 2025

Weekly Market Update: 27 August 2025

Weekly Market Update: 20 August 2025

Weekly Market Update: 13 August 2025

Weekly Market Update: 6 August 2025

Weekly Market Update: 30 July 2025

Weekly Market Update: 23 July 2025

Weekly Market Update: 16 July 2025

Weekly Market Update: 9 July 2025

Weekly Market Update: 2 July 2025

Weekly Market Update: 25 June 2025

Weekly Market Update: 18 June 2025

Weekly Market Update: 11 June 2025

Weekly Market Update: 4 June 2025

Weekly Market Update: 28 May 2025

Weekly Market Update: 21 May 2025

Weekly Market Update: 14 May 2025

Weekly Market Update: 7 May 2025

Weekly Market Update: 27 March 2024

Weekly Market Update: 3 April 2024

Weekly Market Update: 10 April 2024

Weekly Market Update: 17 April 2024

Weekly Market Update: 24 April 2024

Weekly Market Update: 1 May 2024

Weekly Market Update: 8 May 2024

Weekly Market Update: 15 May 2024

Weekly Market Update: 22 May 2024

Weekly Market Update: 29 May 2024

Weekly Market Update: 6 June 2024

Weekly Market Update: 12 June 2024

Weekly Market Update: 19 June 2024

Weekly Market Update: 26 June 2024

Weekly Market Update: 4 July 2024

Weekly Market Update: 10 July 2024

Weekly Market Update: 17 July 2024

Weekly Market Update: 24 July 2024

Weekly Market Update: 31 July 2024

Weekly Market Update: 8 August 2024

Weekly Market Update: 14 August 2024

Weekly Market Update: 21 August 2024

Weekly Market Update: 28 August 2024

Weekly Market Update: 4 September 2024

Weekly Market Update: 11 September 2024

Weekly Market Update: 18 September 2024

Weekly Market Update: 25 September 2024

Weekly Market Update: 2 October 2024

Weekly Market Update: 9 October 2024

Weekly Market Update: 16 October 2024

Weekly Market Update: 23 October 2024

Weekly Market Update: 30 October 2024

Weekly Market Update: 6 November 2024

Weekly Market Update: 13 November 2024

Weekly Market Update: 20 November 2024

Weekly Market Update: 27 November 2024

Weekly Market Update: 4 December 2024